主页 > imtoken官网地址打不开 > NIFD:2021 年人民币汇率回顾和 2022 年展望.pdf 18 页

NIFD:2021 年人民币汇率回顾和 2022 年展望.pdf 18 页

RMB exchange rate Ming Chen Yinmo 2 2 RMB exchange rate, financial supervision, vigilance against the exchange rate of RMB against the US dollar from rising to falling Head of this report: Zhang Ming Summary Author of this report: Zhang Ming Financial Research Institute of Chinese Academy of Social Sciences The RMB exchange rate will show a strong appreciation in 2021 situation. From December 31, 2020, the deputy director of the Institute to December 31, 2021, the central parity rate of RMB against the US dollar rose from 6.5249, deputy director of the National Finance and Development Laboratory to 6.3757, overall Up by 2.3%. During the same period, the exchange rate of RMB against the euro and against the yen appreciated by 10.0% and 12.4% respectively. In the second half of 2021, against the backdrop of the rising U.S. dollar index, the exchange rate of the RMB against the U.S. dollar researcher will still strengthen. This is mainly driven by three factors: First, China's export growth rate continued to remain strong, driving the trade surplus in goods to a new high; second, China's economic recovery after the new crown epidemic was earlier than other countries, and long-term interest rates were significantly higher than those of major developed economies As a result, China is more attractive to short-term capital flows; third, the scale of China's foreign exchange reserves has increased steadily, which has enhanced the confidence of domestic and foreign investors in the RMB exchange rate [NIFD Quarterly Bulletin]. In the global financial market in 2022, considering the repeated high inflation, the Federal Reserve will accelerate the withdrawal of the domestic macroeconomic quantitative easing policy of the RMB exchange rate, and is expected to raise interest rates for the first time in March 2022. China's monetary policy will still adhere to the macro leverage ratio of "maintaining me", which may show a trend of stability and relaxation.

The divergence of the macro-financial monetary policy between China, the US and China is likely to lead to a change in the exchange rate of the RMB against the US dollar. China's financial supervision In 2022, the 10-year US Treasury bond yield will return to 2. above 0%, and even China's fiscal performance may reach 2.4-2.5%. The U.S. dollar index is expected to maintain a high level of local regional fiscal consolidation in the range of 94-102. The pressure of RMB depreciation will increase. The exchange rate of RMB against the US dollar may depreciate to around 6.5-6.6, generally within the range of 6.4-6.6 fluctuation. The bond market, the stock market, the banking industry, the insurance industry, the operation of the insurance industry, the operation of the special assets industry Exchange rate 2 (三) RMB/JPY exchange rate 3 二、 Reasons for stronger-than-expected RMB exchange rate trends in 2021 3 三、 Analysis of future changes in RMB exchange rate in 2022 6 (一) Medium U.S. economic growth gap 6 (二) Sino-U.S. inflation gap 7 (三) Sino-U.S. monetary policy gap 9 (四) Sino-U.S. long-term interest rate changes 10 (五) Global Certainty factors 11 四、 RMB exchange rate trend forecast in 202213 References: 14 一、Characteristic facts of RMB exchange rate movement in 2021 (一) RMB exchange rate against USD in 2021, RMB exchange rate against USD Showing a trend of appreciation amid fluctuations (see Figure 1)). From December 31, 2020 to December 31, 2021, the central parity rate of RMB against the US dollar rose from 6.5249 to 6.3757 , an overall increase of 2.3%.

On December 9, 2021, the exchange rate of RMB against the US dollar rose to the highest point of the year 6.3498. Compared with May 29, 2020, the exchange rate of RMB against the US dollar appreciated by 11%. In 2021, the movement of the RMB against the US dollar exchange rate can be roughly divided into the following two stages: The first stage is from December 31, 2020 to September 30, 2021, when the RMB against the US dollar exchange rate and the US dollar index showed a significant negative relationship. Correlation. During this phase, when the U.S. dollar index goes down, the RMB appreciates against the U.S. dollar, and vice versa. The second stage is from September 30, 2021 to the end of 2021, when the exchange rate of RMB against the US dollar and the US dollar index both show a pattern of rising. From September 30, 2021 to December 31, 2021, the US dollar index rose from 94.2638 to 95.9701, an appreciation of 1.8%; during the same period, the RMB against the US dollar The median price rose from 6.4854 to 6.3757, an appreciation of 1.7%. In 2021, the RMB/CFETS currency basket index will show a continuous upward trend as a whole. From December 31, 2020 to December 31, 2021, the RMB/CFETS currency basket index rose from 94.84 to 102.47, an overall appreciation of 8%. On December 10, 2021, the RMB/CFETS currency basket index reached 102.86, a new high since December 2015 (see Figure 1)).

In the second stage of the RMB/USD exchange rate trend in 2022, that is, in the context of a stronger dollar index, the RMB/USD exchange rate will continue to appreciate. This means that the effective exchange rate of the renminbi against a basket of currencies appreciates faster. From September 30, 2021 to December 31, 2021, the RMB/CFETS currency basket exchange rate index rose from 99.64 to 102.47, an appreciation of 2.8%. 1 Chart of the exchange rate trend of RMB against the US dollar 1 Data source: Wind. (二)The exchange rate of RMB against the euro 20212 In 2020, the trend of the exchange rate of RMB against the euro showed a trend of appreciation in fluctuations (see picture). The central parity rate of RMB against the euro rose to 7.2197, an overall increase of 10%. The trend of the exchange rate of RMB against the euro can be roughly divided into the following two stages: Year, month, day, during this stage, the exchange rate of RMB against the euro showed a trend of 10.7%2021 11 26 appreciation in fluctuations, and the overall value increased; the second stage is year, month, day 20217.1 7.2 To the end of the year, during this period, the exchange rate of RMB against the euro fluctuated slightly within the range of RMB/JPY exchange rate 20213 In 2020, the RMB/JPY exchange rate trend will show a trend of appreciation amid fluctuations (see chart).

12 312021 12 316.3236, the central parity rate of the RMB/JPY exchange rate rose to 5.5415, an overall appreciation of 12.4% during the year. In 2021, the movement of the RMB against the Japanese yen exchange rate can be roughly divided into the following three stages: the first 2020 12 31 2021 6 4 stage is from the year-month-day to the year-month-day. During this stage, the exchange rate of RMB against the yen 8.1% 2021 6 42021 The rate shows an appreciation trend, and the overall value has risen; the second stage is from the year-month-day to September 22. During this stage, the exchange rate of RMB against the yen showed a small fluctuation characteristic. RMB5.8 5.92021 9 22 The exchange rate against the Japanese yen fluctuates slightly within the range of to; the third stage is from the date of the year to the end of 2021. Turning to a rapid appreciation trend, the overall increase in this stage is 6.4%. Figure 3 The data source of the exchange rate trend of RMB against the Japanese yen: Wind. 二、The reasons for the stronger-than-expected RMB exchange rate trend in 2021 In the article "Beware of the Potential Negative Impact of the Inversion of the Growth Gap between China and the U.S." in the RMB exchange rate analysis report for the third quarter of 2021, the author, based on the differences in economic growth rates between China and the U.S., Analysis of the RMB exchange rate trend in the fourth quarter of 2021 from four dimensions: the difference in U.S. inflation, the difference in monetary policy between China and the U.S., and the change in long-term interest rates between China and the U.S. The author predicts that, affected by the reversal of the economic growth gap between China and the United States, it is expected that by the end of the fourth quarter of 2021, the US dollar index may show a moderate strengthening trend, generally operating in the range of 93-95; the exchange rate of the RMB against the US dollar may depreciate to 3 < Around @6.5-6.6, the general fluctuates in the range of 6.4-6.7.

From a practical point of view, the trend of the US dollar index is basically in line with the author's expectations. The US dollar index rose from 94.0747 on October 1, 2021 to 95.9701 on December 31, 2021. The most important reason for the significant rise in the US dollar index in the fourth quarter of 2021 is that Stimulated by the unprecedented expansionary policy,the domestic inflation rate in the United States has recently hit a new high预测2022年的美元汇率, and the Federal Reserve has to start the normalization of monetary policy. The normalization of monetary policy will undoubtedly lead to an increase in short-term and long-term interest rates in the United States, which will push the dollar index up. When the U.S. dollar index rises, the yuan usually depreciates against the U.S. dollar. However, the trend of the exchange rate of RMB against the US dollar did not develop according to the logic deduced by the author. In the fourth quarter of 2021, against the backdrop of the upward trend in the US dollar index, the exchange rate of the RMB against the US dollar will continue to appreciate. The author believes that there are three reasons behind this. One of the reasons: In the second half of 2021, China's export growth continued to remain strong, driving the trade surplus in goods to a new high, while the trade surplus drove the strengthening of the RMB exchange rate (see Figure 4). From August to 2021) In October, the monthly year-on-year growth rate of China's exports in US dollar terms exceeded 25% for three consecutive months, and the trade surplus in goods for these three months continued to rise, reaching 584、668 and 84.5 billion US dollars respectively. 84.5 billion US dollars or even It has set a new record for China's monthly trade surplus in goods. In fact, in the first half of 2021, due to the base period effect, China's exports have already experienced ultra-high growth. Originally, the market expected that the export growth rate would drop significantly in the second half of 2021. The global epidemic has intensified again, especially the impact of the significant intensification of the epidemic in Southeast Asia, and the indispensableness of China's exports has once again increased, thus promoting the continued strong export growth rate.

According to WTO statistics, in 2021, the share of China's exports in global exports will increase substantially, reaching 16.7%. In 2021, China's annual exports will be as high as 3.$36 trillion, far exceeding the combined export share of the United States and Germany (about 3.$24 trillion). In 2021, China's booming external sector and a stable balance of payments structure have accumulated sufficient US dollar liquidity for the inter-bank market, strong demand for RMB in the foreign exchange market, and strong demand for foreign exchange settlement dominates the strong trend of the RMB exchange rate (Wei Wei). And Guo Zirui, 2022). 4 Figure RMB real effective exchange rate index and China’s export growth year-on-year 4 Data source: Wind. Reason 2: Because China’s economic recovery after the new crown epidemic is earlier than other countries, and China’s long-term interest rate Significantly higher than major developed economies, making China more attractive to short-term capital flows. The surplus in trade in goods combined with cross-border capital inflows make China generally face net cross-border capital inflows. For example, July-September 2021 The surplus of foreign exchange settlement and sales by banks on behalf of customers was 129、181 and 26.8 billion U.S. dollars, respectively, with a total of 57.8 billion U.S. dollars in three months, significantly higher than the 10.7 billion U.S. dollars in the same period of 2020 and -13.2 billion U.S. dollars in the same period of 2019. In December 2021, the surplus of foreign exchange settlement and sales by banks on behalf of customers was as high as US$51.6 billion (see Figure 5)). The net inflow of cross-border capital means that there is an oversupply of US dollars in the domestic foreign exchange market, which will also promote the exchange rate of RMB against the US dollar. Appreciation. Figure Bank valet foreign exchange settlement and sales surplus 5 Data source: Wind.

5 Reasons 3: The scale of China's foreign exchange reserves has been rising steadily, which has enhanced the confidence of domestic and foreign investors in the RMB exchange rate. From 2017 to 2020, the monthly average size of China’s foreign exchange reserves was 3.07、3.11、 3.10、3.13 trillion US dollars (see Figure 6)). From January to October 2021, the monthly average size of China’s foreign exchange reserves reached 3.21 trillion US dollars, significantly higher than the average of previous years In particular, it is worth mentioning that due to the general strengthening of the US dollar index in 2021 YTD, this will have a negative valuation effect on China's foreign exchange reserves. Against this background, the scale of China's foreign exchange reserves in December 2021 will be as high as 3. US$25 trillion, which is a new high since January 2016, indicating that the flow of foreign exchange reserves may grow faster. Figure 6 The scale of China's foreign exchange reserves Data source: Wind. 三、The future of RMB exchange rate in 2022 To analyze and judge the trend of RMB exchange rate in the next stage, it is necessary to compare the economic fundamentals of China and the United States and the trend of monetary policy between China and the United States, and consider the disturbance of global uncertainties. Monetary policy differences, changes in long-term interest rates between China and the United States, and global uncertainties will be analyzed separately. (一)The difference in economic growth between China and the United States The U.S. GDP growth rate in 2021 is 5.7% , China’s GDP growth rate is 8.1%. Yu Yongding (2022) pointed out that if the base effect is deducted, China’s economy in 2021 will run at a level lower than 6% in 2019.

In January 2022, the IMF’s latest World Economic Outlook lowered the U.S. GDP growth rate in 2022 from 5.2% to 4%, mainly considering that the U.S. Congress passed the “Building a Better Future” Act, a fiscal package. The likelihood of measures has declined, the authorities have withdrawn from unconventional accommodative monetary policy earlier, and the economy faces persistent supply6 disturbances. At the same time, the IMF lowered China's GDP growth rate in 2022 from 5.6% to 4.8%, considering the continued contraction of China's real estate sector and the weaker-than-expected recovery of private consumption. 1 In 2021, the US quarterly GDP growth rates will be 0.5%, 12.2%, 4.9%, and 5.5%, respectively. China's quarterly GDP growth rates were 18.3%, 7.9%, 4.9% and 4.0%, respectively. In contrast, in the second quarter, the U.S. quarterly GDP growth rate exceeded that of China; in the third quarter, the U.S. GDP growth rate was basically the same as that of China’s GDP; in the fourth quarter, the U.S. GDP growth rate was better than that of China’s GDP (see Figure 7). In the figure, the year-on-year growth rate of GDP in the US quarterly 7. Source: Wind. (二)Inflation difference between China and the US 20218 2021 12021 In 12 years, the US inflation rate continued to rise (see figure). Year month By 2019, CPI 1.4%782 7 The U.S. rose rapidly from 2009 to 2010, which is the highest inflation level in the United States since 2008. During the same period, the year-on-year growth rate of core CPI increased from 1.4% to 5.5%.

There are three reasons for the rapid rise in the inflation rate in the United States: First, because the macro policy stimulus in the United States is biased towards the demand side (such as a large-scale fiscal payment to low- and middle-income households), the recovery of the domestic demand side in the United States is significantly faster than that of the supply side. Second, the global outbreak of the epidemic has led to a significant decline in the supply and long-distance transportation of bulk commodities, pushing up global commodity prices. Third, under the premise that the US economic growth has recovered significantly, the US government's fiscal and monetary policy has lagged significantly. With U.S. inflation hitting record highs, the Fed had to start normalizing monetary policy. 1 Source: World Economic Forecast for January 2022, IMF Public Account, January 25, 2022. 7 Figure U.S. 8CPI and core CPI data source: Wind. In 2021, China's inflation rate will be generally controllable, and the CPI growth rate will remain at a low level (see Figure 9)). From January 2021 to December 2021, the year-on-year growth rate of China's CPI will increase from -0.3% Rising to 1.5%. The trend of China’s CPI is basically in line with the author’s expectations in the analysis report of the RMB exchange rate in the third quarter of 2021. In 2021, the trend of China’s PPI peaked and fell, but the rate of decline was not as fast as the author expected. January 2021 By December 2021, the year-on-year growth rate of China's PPI will soar from 0.3% to 10.3%. In October 2021, the year-on-year growth rate of China's CPI and PPI will increase to 1.@ >5% and 13.5%, the gap between the two has reached a historic peak.

The main reason for the soaring year-on-year growth of China's PPI is the rise in global commodity prices. At present, the prices of many types of commodities have hit record highs. The rise in global commodity prices has created significant imported inflationary pressures on commodity-importing countries. In 2021, the general domestic commodity price index, energy price index, steel price index and agricultural product price index will all hit record highs. In October 2021, the year-on-year growth rate of China's import price index is as high as 17.0%. The author believes that the probability of commodity prices reaching new highs in 2022 will be significantly lower than the probability of falling back from highs. In particular, those commodities that are deeply hyped by financial capital will face high volatility in prices in 2022. To this end, the price trend for a period of time in the future will show a pattern of moderate growth in China's CPI year-on-year growth rate and a drop in PPI year-on-year growth rate. 89CPI PPI graph China and data source: Wind. (三)The difference in monetary policy between China and the United States The Federal Reserve began to withdraw from the quantitative easing policy. After the outbreak of the new crown epidemic, the US government implemented an unprecedented and extremely loose fiscal and monetary policy. In terms of fiscal policy, in 2020, the federal government’s fiscal deficit accounted for GDP The ratio reached 14.9%, significantly higher than the 9.8% in 2009 after the subprime mortgage crisis broke out. In 2020, the federal government debt-to-GDP ratio increased by 24.3 percentage points ,reaching 132.5%. In terms of monetary policy预测2022年的美元汇率, in addition to implementing zero interest rates again, the Fed has also implemented a huge quantitative easing policy.

In less than two years, the total size of the Fed's balance sheet has more than doubled, from $4 trillion to nearly $9 trillion. Stimulated by the easing policy, the inflation situation in the United States has deteriorated significantly. Although the inflation rate began to rise significantly in the first half of 2021, the Fed believes that this is only a temporary disturbance, and the inflation rate will naturally decline as production recovers and the gap between supply and demand disappears. However, various pressures caused by the continued rapid rise in inflation in the second half of 2021 still led the Fed to make policy revisions in early November 2021, announcing that it will begin to reduce the scale of quantitative easing. Luo Zhiheng and Fang Kun (2022) pointed out that the Fed’s raising interest rates to fight inflation is not only an economic demand, but also political pressure; the inflation problem has plagued the Biden administration, and the public opinion rate has hit a record low, and the Biden administration will actively support the Fed Raise interest rates to fight inflation. From November 2021, the Fed will reduce bond purchases by $15 billion per month, which means that the Fed will stop quantitative easing at the end of June 2022. In January 2022, the Fed announced that it will accelerate the reduction in purchases The speed of debt, the Taper will be completed in March 2022, and the interest rate hike will basically start. Zhang Yu and Yin Wenqing (2022) pointed out that in terms of the current inflation and employment gap that the Fed is concerned about, there are conditions for three interest rate hikes in 2022. 9 The true speed of the Fed’s exit from quantitative easing monetary policy will bring uncertainty to the global economy in 2022. Historically, emerging markets and developing countries will face massive short-term capital outflows whenever the Fed enters a cycle of monetary policy tightening , The local currency exchange rate is facing depreciation pressure, the price of domestic risk assets has fallen, and the domestic economic growth has slowed down.

In severe cases, it may even lead to currency crises, debt crises, financial crises and even economic crises. If the Fed tightens monetary policy faster than the market expects, the external negative shocks faced by emerging markets and developing countries will be more severe. Taking history as a mirror, in 2022 and 2023, the Fed's new round of monetary policy normalization may cause some emerging market economies to suffer serious negative impacts. And the hit will be particularly severe for countries that run persistent current account deficits, borrow large amounts of foreign debt, and rely heavily on capital inflows. For China's economy, the growth rate of China's economy in 2021 will be high and then low, and the monetary policy will strengthen the cross-cycle adjustment based on the changes in the economic situation in the first and second half of 2021 (Sun Guofeng, 2022). July 2022 And in December, the People's Bank of China implemented two comprehensive RRR cuts of 0.5 percentage points each. Considering that China's current overall inflation situation is controllable, prices are not the reason for accelerating the normalization of monetary policy. In 2022, the People's Bank of China will adhere to stable Taking the lead, seeking progress while maintaining stability, taking the responsibility of stabilizing the macro economy, and proactively launching a monetary policy that is conducive to economic stability (Sun Guofeng, 2022). Considering that China’s economic GDP growth rate will still be relatively large in 2022) Downward pressure, China's monetary policy may show a stable and loose trend. (四)The change in long-term interest rates in China and the United States may lead to the withdrawal of the Fed's quantitative easing policy, which may lead to a rise in US bond yields, and the US dollar index may still be at a high level 100.@ >5%. After the outbreak of the new crown epidemic, the yield on the one-year US Treasury bond once fell to a historic 2021 121.5%2013 low.

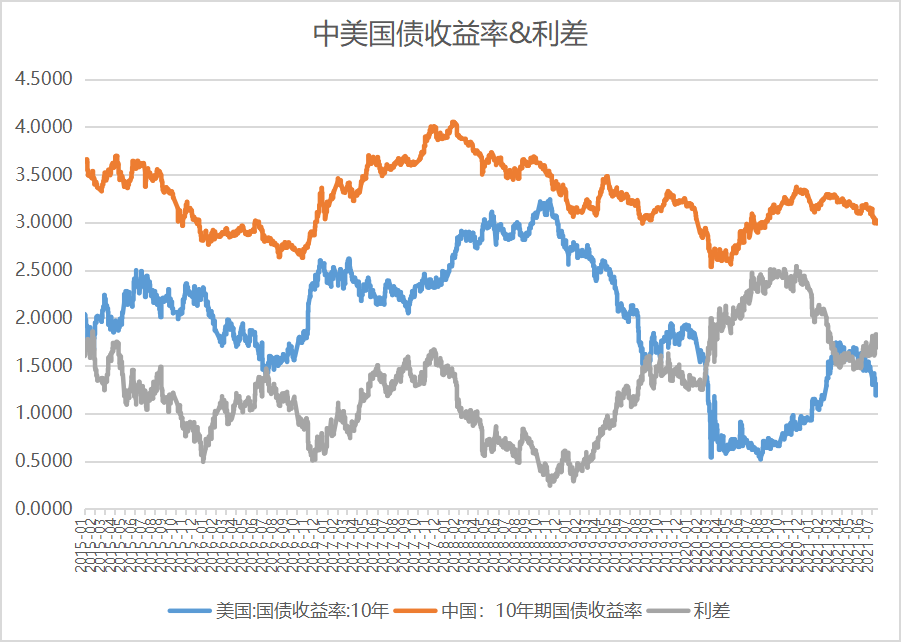

As of late December, the indicator has rebounded to . During the Fed's last Taper101.5%3% period in 2018, the one-year U.S. Treasury bond yield rebounded from left to right to above, and then fell back in 2015-2018. As the Fed continues to raise interest rates from year to year, the yield on one-year US Treasury bonds has rebounded to above 3.0%202210 degrees. The author believes that in 2018, the Fed's exit from quantitative easing will bring the yield of the one-year US Treasury bond back to 2. above 0%, and may even reach 2.4-2.5%. This means that the US bond 103 market will face some downward pressure. After the outbreak of the new crown epidemic, the U.S. dollar index first touched a high, and then fell to the vicinity of 90202196-972022, and then rebounded to around the current level in the second half of the year. The author believes that in 2019, considering the normalization of the Fed's monetary policy, the US dollar index is expected to consolidate at a high level within the range of 94-102. 102021 In stark contrast to the upward trend in US bond yields, the one-year Chinese government bond yields are on a downward trend in 10-year fluctuations (see Figure 10). From January 4, 2021 to December 2021) On the 31st, the yield of 10-year Chinese government bonds fell from 3.1713% to 2.8352%, a decrease of 33 basis points. During the same period, the yield spread of 10-year Chinese government bonds between China and the United States dropped from 2.@ >2413% narrowed to 1.3152%. With the pace of interest rate hikes by the People’s Bank of China since December 2021, the yield of 10-year Chinese government bonds dropped to <@ on January 25, 2022.2.6938%.

The narrowing of the interest rate gap between China and the United States will affect short-term cross-border capital flows, which in turn will affect the demand for RMB exchange rate transactions, thereby affecting the RMB exchange rate trend. In the short term, China will face certain pressure from capital outflows. Figure 10 China-US interest rate spread data source: Wind. (五)Global Uncertainty Factors In addition to the uncertainty that the U.S. monetary policy shift will bring to the global economy, the global economic growth in 2022 will also be disturbed by two major uncertainties, which will increase the RMB exchange rate Uncertainty of future changes. One of the uncertainties is that the duration and intensity of the new crown epidemic has once again exceeded expectations. At the beginning of 2021, with the launch of effective vaccines worldwide, the market generally believes that by the second half of 2021, the epidemic will Delta will be fully controlled in 2021. But what I didn't expect is that in 2020, the new coronavirus variant Delta ( ) once again ravaged the world, causing the global epidemic prevention and control situation to become serious again. At the end of 2021, Omicron WHO2022 1Omicron was found in South Africa. The latest variant of the virus. Data shows that as of the beginning of this year, it has spread to at least 128 countries. Relevant studies have shown that compared with previous strains, Omicron is more resistant to antibodies and is more resistant to existing vaccines. From the current point of view, the global evolution of the new crown epidemic in 2022 is not optimistic, especially for developing countries (especially African countries) whose vaccine injection progress is lagging. If the new crown epidemic continues to rage, then the global economy in 2022 will be affected. The growth rate may not be as high as expected.

The second uncertainty is rising global geopolitical risks. In 2021, against the backdrop of the ongoing COVID-19 crisis, global geopolitical risks are intensifying. From the perspective of the geopolitical risk index, from July to December 2021, the global geopolitical risk index rose rapidly from 59.16 to 99.99 (see Figure 11). 2021 In 2020, Sino-U.S. frictions, the civil unrest in Kazakhstan, and the withdrawal of U.S. troops from Afghanistan all increased global geopolitical risks. In 2022, special attention should be paid to the evolution of the Russia-Ukraine conflict and Sino-U.S. friction. The upgrade in 2022 will not only undermine the regional security situation, but also affect the global energy supply and energy transition, and have a chain reaction on the foreign policies of Central and Eastern European and Central Asian countries (Institute of World Economics and Politics, Chinese Academy of Social Sciences, 2022). As far as Sino-US frictions are concerned, the Biden administration will continue the Trump administration's China policy in 2021, regard China as the biggest challenger and competitor of the US, and gradually expand high-tech sanctions against China, etc. Measures to suppress China (Gao Jianbo et al., 2022). Shannon K. O'Neil, vice chairman of the Council on Foreign Relations of the United States, pointed out that geopolitics and government activism are the main factors affecting the next stage of globalization, while It is not trade, investment or the spread of the virus, the worsening of Sino-US political tensions will continue. 2 Figure 11 Global Geopolitical Risk Index Data Source: /gpr.html. 2 Source: 12 Top Experts including Joseph Nye: Covid-19 The epidemic has resumed in a year, where will the "post-epidemic era" go?", Guozheng Scholar's official account, January 9, 2021.

/2021/01/02/2021-coronavirus-predictions-global-thinkers-after-vaccine/12四、2022 RMB exchange rate forecast 202210 Looking ahead, the Fed's withdrawal from quantitative easing monetary policy will make the US Treasury yields are back above 2.0%, and may even reach 2.4-2.5%. This means that the US bond market will face some downward pressure. With the progress of the normalization of the Fed's monetary policy, the US dollar index still has some room for moderate upside. The author believes that the US dollar index is expected to consolidate at a high level in the range of 94-102 in 2022. CFETS2015 12 Considering that the RMB against the currency basket index is currently at a new high since 2015, it is expected that the room for continued appreciation of the RMB effective exchange rate in the next stage is relatively limited. Under the external environment of the Fed's continued tightening of monetary policy, in order to boost domestic economic growth and prevent and control systemic financial risks, China's monetary policy is marginally relaxed, then the exchange rate of RMB against the US dollar is expected to decline moderately. The author predicts that in 2022, the exchange rate of RMB against the US dollar may depreciate to around 6.5-6.6, and generally fluctuate in the range of 6.4-6.6. 13 References: 1. Gao Jianbo, Ding Yupei, He Xin, He Zhaoyang, Hou Xin, Hu Qiyue, Liu Bin, Sun Xiaohui, Wang Fang2022 Lei, Zhang Wei, Wang Meng: “Top Ten Global Conflicts or Crises and Development Trends” Prospects,” Cultural Aspects, 2022.

2. Luo Zhiheng, Fang Kun: "Rising waves, comments on the Fed's monthly interest rate meeting", Yuekai Securities, 120221 27-month-date. 3. Sun Guofeng: Review and Prospect of Monetary Policy, China Finance, No. 2022. 34.2022 Wei Wei and Guo Zirui: "Annual Foreign Exchange Market Outlook for RMB: Two-way Fluctuation, Return to Neutrality", 2022 16 Ping An Securities, dd. 5. Yu Yongding: "Fourteen Viewpoints on the Macroeconomics in 2022", China Finance Forty Forum, January 25, 2022. 6. Zhang Yu and Yin Wenqing: "The Fed's "big stance" is fully demonstrated. What are the support and constraints for raising interest rates this year? ——1 Comments on the 1 FOMC2022 January 27 Meeting”, Huachuang Securities, dd. 7. Institute of World Economics and Politics, Chinese Academy of Social Sciences, Chinese Academy of Social Sciences National Global Strategy 20222022 1 14 12 Think Tank: "Top Ten Global Potential Risks in 2020", "Guangming Daily", dated edition. Copyright Notice: [NIFD Quarterly Bulletin] is copyrighted by the National Finance and Development Laboratory. Without the permission of the copyright owner, no institution or individual may reproduce, copy, go online or publish in any form. If there is any violation, the copyright owner reserves the right to follow up liability rights. The report reflects only the views of the original authors and does not represent the views of the copyright owners or their affiliations. Production unit: National Finance and Development Laboratory. 14